Yesterday we talked about Money Madness and how it all begins by losing perspective on the role money should play in your life and your marriage. Over the next couple of days (or however long), I want to provide you with some tools to help keep your perspectives in their proper place and to help you manage the money madness.

Tool Number One: Budgeting

Many of us have heard about budgeting and that it's important, but if you're like me I never actually knew how to set up a budget that works until a little over two years ago. Having a plan in place has tremendously reduced the money stress for Jimmy and I. It's not that we make more; it's just that we are better stewards of the money God has given us because we now have a plan in place to help us accomplish our goals.

What is Budgeting?

According to

Dictionary.com these are just some of the definitions of the word "Budget".

Budget –noun

| 1. | an estimate, often itemized, of expected income and expense for a given period in the future. |

| 2. | a plan of operations based on such an estimate. |

| 3. | an itemized allotment of funds, time, etc., for a given period. |

| 4. | the total sum of money set aside or needed for a purpose: the construction budget. | | | | |

In Christiana terms, a budget is my plan for what to do with my money this month. Now that we have talked about what a budget is, we can talk about how to make a budget.

Making a Simple Budget

One of the things that helped Jimmy and I to get our finances on track was taking one of Dave Ramsey's Financial Peace University (FPU) classes. The course covers all the basics of budgeting, getting out of debt, planning for the future, investing, and more. It was a very useful class so I want to pause a moment and give you some links to more information about FPU and Dave Ramsey. If you want to know more about Dave Ramsey,

click here. If you would like more information about an FPU class in your area,

click here. Part of the reason I wanted to give you these links is because Dave has really helped us and part of it is because I want to refer you to Dave's simple budgeting forms to help you make your own plan.

Step One: Figure out How Much You Make Each Month

Add up all income sources for you and your spouse to get the total amount of income you will have for the month. I know that this is trickier for some because you are not salaried or you might work on commission. If you are in these situations, I would base your total income off an average of your income for the last few months. This might take a little research on your part but you can do it!

Step Two: List all Your Bills and Expenses for the Month

The first part is easy. Most of us know which bills we have to pay every month and about how much they are going to cost. So write them all out (I would also make a note of when payment is due--we will use this later). Now that you have listed rent/house payment, car payments, cell phones, internet, cable, credit card payments, school loan payments, etc. It's time to work on the expenses. This is a little tricky and may take some estimating. Do the best you can in estimating how much you spend on clothing, hair cuts, toiletries, medications, gas, food, etc. Don't worry you will probably change this later anyway, so just give your best estimate for now.

Step Three: Make Your Budget

Now this is the truly hard part. It's not that the dividing of funds is hard. It's seeing just how out of whack our finances can be that is hard.

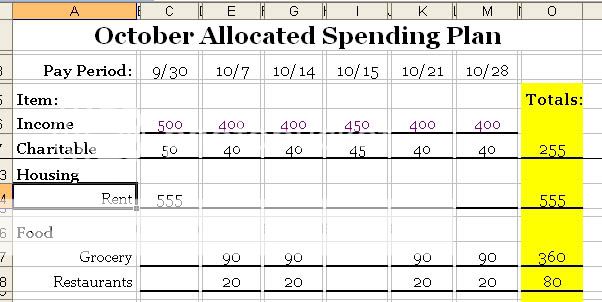

CLICK HERE for Dave's downloadable budget forms. They are easy to use and they can help you to think of areas you might have missed.

A COUPLE OF NOTES

*Your budget

WILL NOT be perfect the first time! Dave estimates that it takes 3 to 4 months for you to get most of the bugs worked out of your budget.

*Your budget

MOST LIKELY will change each month although some items will remain the same.

*The key to a successful budget it to

PLAN AHEAD. You might not need to have any car repairs done this month, but if you plan ahead and budget $20 a month for car repairs that you save until you do need them then when your car breaks down and costs $400 to fix it won't be nearly as stressful because you have been saving money toward such an event.

Now back to making your budget. The best option is to make what is called a zero based budget. This means that you plan for ALL money you make with a remainder of $0 unplanned. This means that you will even plan how much spending money you and your spouse will get to do whatever you want with it. I suggest that you start filling in the form by writing in your necessities housing, food, transportation, etc. Then work on your other priorities such as bills. Finally, use the remainder for savings, spending, etc.

NOTE: DON'T FORGET TO TITHE! I personally believe that this should be #1. Jimmy and I have found that when we commit to giving God His money first, we will always have enough to pay for our necessities even if we don't always know where the money is going to come from.

Give It a Go!

So take some time and have a "budget meeting" with your spouse. Do your best to estimate your income and expenses. If you need helps or have comments/questions, feel free to come back and post or you can look for answers on

Dave Ramsey's Website. Happy budgeting!